New Merger Guidelines Reflect Agencies’ Aggressive Enforcement Stance

On December 18, the Federal Trade Commission and the Department of Justice (together, “the Agencies”) jointly issued their 2023 Merger Guidelines,1 which describe the factors the Agencies consider when reviewing mergers and acquisitions. It follows a long practice of the Agencies issuing such guidance, with versions dating back to the 1980s.

The 2023 Guidelines reflect the analytical framework that the Agencies have been applying since the start of the Biden Administration. As such:

- They provide greater transparency into the Agencies’ thought processes, which companies and their counsel can use as they assess and allocate risk of an Agency investigation into potential deals.

- Parties to a transaction subject to Agency scrutiny can tailor their presentations of evidence and economic analysis, allowing parties to address theories head-on and engage in a more meaningful dialogue.

- Courts, though, remain the ultimate arbiter of whether a deal violates the law. Although courts have long relied upon the Agencies’ Guidelines in merger review cases, the extent to which courts will apply the 2023 Guidelines remains to be seen.

- Although many aspects of the 2023 Guidelines reflect existing consensus on antitrust principles, informed by the Agencies’ experience, other aspects are subject to ongoing debate. Just as the Biden Administration FTC rescinded the joint FTC/DOJ 2020 Vertical Merger Guidelines upon taking office, future administrations may modify these 2023 Guidelines.

The 2023 Guidelines reflect the Biden Administration’s goal of aggressively enforcing the antitrust laws. Soon after taking office, President Joe Biden issued his “Executive Order on Promoting Competition in the American Economy” that directed a “whole-of-government approach” to address what the Administration described as the problem of “excessive market concentration.”2 Since that time, the Agencies have become increasingly active in developing theories of harm and bringing court cases to challenge mergers (with varying degrees of success).

The 2023 Guidelines are yet another step in this effort to drive a “national policy to promote open and fair competition.” (Guidelines at 1.) Indeed, FTC Chair Lina Khan emphasized that “policing unlawful mergers is our front line of defense against harmful corporate consolidation.”3

In addition to the 2023 Guidelines, the Administration is also finalizing proposed revisions to the pre-merger notification (“HSR”) filing requirements. Assuming the final rule matches the notice of proposed rulemaking issued earlier this year, the revisions will fundamentally transform the HSR process. Parties to every HSR-reportable transaction will be required to provide—up front—detailed narratives about their deals, extensive amounts of documents and information (including about employees), and reams of data.4

Merging parties should view these two efforts as complementary pieces of the Administration’s merger review playbook, with the HSR revisions affecting process and the Guidelines addressing substance.

Unlike the HSR rules, the Guidelines are not legally binding. Instead, they reflect the Agencies’ current views on how they assess mergers. The Agencies cannot themselves block a transaction. They must bring suit and convince a federal judge that a proposed deal violates the law. Many courts have favorably cited past versions of the Guidelines, relying upon them for an analytical framework, given the dearth of Supreme Court merger cases over the past fifty years.5 It remains to be seen if courts will treat the 2023 Guidelines similarly.

While a full discussion of the numerous legal and economic theories raised in the 2023 Guidelines is beyond the scope of this alert, the key takeaways for dealmakers to consider are:

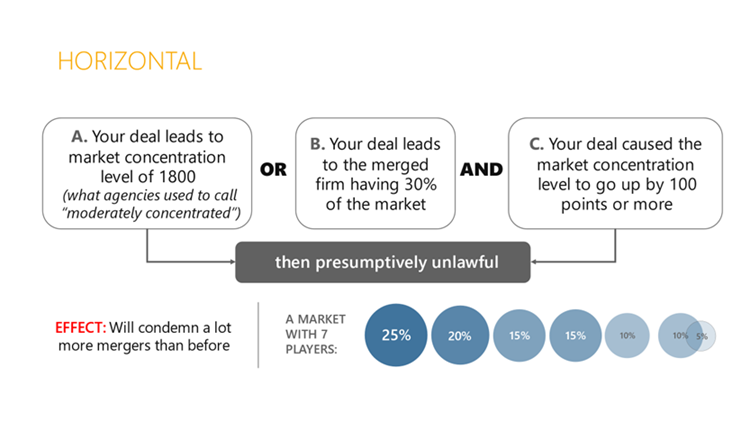

1. Lower thresholds for a “presumption” of harm. Perhaps the most important change in the 2023 Guidelines—compared to prior practice—relates to the thresholds at which transactions are presumed to raise competitive concerns. The government can establish a presumption of harm by showing that a transaction will lead to undue concentration in the market. The 2023 Guidelines lower the HHI-based threshold6 for the Agencies to presume a deal is anticompetitive to levels found in the 1992 Guidelines (those levels had been raised in the 2010 Guidelines).

The Agencies now assert that a transaction should be presumed to be harmful if (1) the post-merger market-wide HHI is greater than 1,800, and the change in HHI from the transaction is greater than 100 points, or (2) the merged firm’s market share is greater than 30%, and the change in HHI is greater than 100 (2023 Guidelines at 6).

The upshot is that the lower thresholds will ensnare more deals. For example, the Agencies will view a transaction in which one party has a market share as low as 30%, and the other party has a relatively small share (e.g., 2%), as presumptively illegal.

However, dealmakers should know that context is critical when considering “presumptions” of harm:

- A presumption is only as good as the market on which it is based. The definition of the relevant market is, of course, critical to determine market shares. Most antitrust merger cases turn on disputes about whether the relevant market is narrow (where the parties’ shares are likely high) or broad (and the concomitant shares lower).

- A presumption is just a presumption; it does not mean that a deal is illegal. The merging parties can rebut the presumption with evidence showing why the merger is unlikely to harm competition. See United States v. Baker Hughes, 908 F.2d 981, 991 (D.C. Cir. 1990). The initial public draft version of the 2023 Guidelines was ambiguous about rebuttal evidence; the final version now explicitly states: “This presumption of illegality can be rebutted or disproved.” (2023 Guidelines at 6.)

- The effect of the presumption can be overstated. The burden-shifting framework for merger reviews is applied “flexibly” with “evidence considered all at once and the burdens are often analyzed together.” Illumina, Inc. v. Fed. Trade Comm’n, No. 23-60167 slip op. at 9 (5th Cir., Dec. 15, 2023) (internal citation omitted). In practice, the commercial realities drive the result based on analysis of marketplace facts, not formulaic presumptions.

Accordingly, while these presumptions are important, they are not determinative.

2. An increased emphasis on vertical mergers. The 2023 Guidelines are the first set of Agency merger guidelines that address both horizontal (direct competitor) and vertical (different levels of supply chain) deals in the same document. The Administration has been clear about wanting to challenge more vertical transactions in order to advance the law in this area, and the 2023 Guidelines reflect that position as they contain a detailed section describing how mergers can create a firm that may limit access to products or services that its rivals use to compete. The Guidelines set forth the well-accepted “ability and incentive” framework to analyze such “foreclosure.” But they also assert the so-called Brown Shoe framework—examining industry factors and market structure—as an alternative basis for foreclosure liability. Recent courts have been reluctant to fully endorse such a framework.7 We expect the Agencies will use the Guidelines to try to push courts to more forcefully adopt this approach.

3. Emphasis on Labor Markets. Courts and enforcers have long recognized that businesses compete not only for “downstream” sales to customers but also for “upstream” purchases of inputs. A centerpiece of the Administration’s antitrust push has been to emphasize that antitrust laws protect labor. The Guidelines have an entire section focused on assessing whether a merger affects competition for workers, creators, suppliers, or other providers. This is an area that is not developed in the caselaw as no court has addressed the impact of mergers on competition for employees.8 As such, there are many open questions relating to defining labor markets and assessing the impacts of mergers on workers. The Guidelines stake out the position that labor markets “frequently have characteristics that can exacerbate the competitive effects of a merger between competing employers” and that “labor markets can be relatively narrow.” (Guidelines at 27.) The Agencies will surely be testing such theories in future merger reviews and perhaps litigated cases.

4. Serial Acquisitions & Trends toward Concentration. The 2023 Guidelines stake out the position that a particular merger should not be examined in isolation when it is one in a series of acquisitions (such as a roll-up) or there otherwise is a trend toward concentration. In such situations, the Agencies state that they will consider the collective or cumulative effect of the pattern of acquisitions. As part of this consideration, the Agencies explicitly warn against parties engaging in an “arms race” for bargaining leverage:

The Agencies sometimes encounter mergers through which the merging parties would by consolidating, gain bargaining leverage over other firms that they transact with. This can encourage those other firms to consolidate to obtain countervailing leverage, encouraging a cascade of further consolidation. This can ultimately lead to an industry where a few powerful firms have leverage against one another and market power over would-be entrants or over trading partners in various parts of the value chain.

(Guidelines at 22.9) A difficult line-drawing exercise will occur in these “serial” fact patterns; i.e., are there situations where the Agencies will challenge a specific deal that does not in isolation raise a competition concern but might be part of a pattern? For example, is there competitive harm if two small companies want to merge to gain bargaining power against a large supplier? If so, what standards should apply?

5. Rebuttal Evidence/Efficiencies. Section IV of the Guidelines discusses certain types of rebuttal evidence that parties can employ to show that a merger does not threaten a substantial lessening of competition, including “failing firm,” ease of entry/repositioning, and procompetitive efficiencies. The Agencies stress that, while they recognize these defenses, they will place a high burden on the merging parties to substantiate any such claims.

One change from the 2010 Guidelines is particularly telling as to the current Administration’s views on efficiencies compared to its predecessors. Footnote 14 from the 2010 Guidelines explained that, in some cases, the Agencies “will consider efficiencies not strictly in the relevant market, but so inextricably linked with it that a partial divestiture or other remedy could not feasibly eliminate the anticompetitive effect in the relevant market without sacrificing the efficiencies in the other market(s).”10 This footnote was a concession toward pragmatism in that some mergers are likely to offer great efficiencies to customers outside a relevant market but may have a small anticompetitive effect in a relevant market (and that harm could not be cured by divestiture). Overall, the merger would benefit customers. In past administrations, the Agencies exercising their prosecutorial discretion could clear such a merger. The current Administration takes the view that such mergers are illegal and must be challenged.

Closing Thoughts

The 2023 Guidelines constitute 51 dense, single-spaced pages, covering myriad legal and economic theories of harm. The discussed points are just the tip of the iceberg, with the Guidelines further providing the Agencies’ views on topics such as mergers that:

- eliminate potential entrants;

- entrench or extend a dominant position;

- involve multi-sided platforms or cluster markets; and

- partial ownership/minority interests (of particular relevance for private equity investors that acquire interests in competing companies through different funds).

Each of these areas raises complex issues. One of the goals of the 2023 Guidelines is transparency; as such, one benefit of the Guidelines is that they provide, in writing, the analytical framework and assessments that the Agencies themselves have been operating under since the outset of the Biden Administration. As a result, antitrust practitioners will be able to address these theories during merger reviews to engage in a meaningful dialogue, to hopefully reach an amicable outcome with the Agencies. Failing that, the courts remain the ultimate arbiter of whether a deal violates the law.

1 2023 Merger Guidelines, Dep’t of Just. and Fed. Trade Comm’n, Dec. 18, 2023, https://www.justice.gov/atr/2023-merger-guidelines.

2 Executive Order on Promoting Competition in the American Economy | The White House, Exec. Order No. 14,036, 86 C.F.R. 36987 (July 9, 2021).

3 Federal Trade Commission and Justice Department Release 2023 Merger Guidelines, Fed. Trade Comm’n, Dec. 18, 2023, https://www.ftc.gov/news-events/news/press-releases/2023/12/federal-trade-commission-justice-department-release-2023-merger-guidelines.

4 For more details about this proposed rule, please see The FTC’s Proposed HSR Changes: What They Mean for Dealmakers | Perspectives & Events | Mayer Brown.

5 The 2023 Guidelines cite to many Supreme Court merger cases from the 1960s and early 1970s, stressing that “legal holdings reflecting the Supreme Court’s interpretation of a statute apply unless subsequently modified.” (2023 Guidelines at 4.) At the same time, however, the Agencies assert that they are not constrained by how the Court applied the law to the facts of those cases: “References to court decisions do not necessarily suggest that the Agencies would analyze the facts in those cases identically today.” Id.

6 The Herfindahl-Hirschman Index (HHI) of market concentration consists of the sum of the squares of the market shares of the competitors in the relevant market. The change in the HHI measures the impact of a merger, in terms of the shares of the merging competitors.

7 See, e.g., Concurring Opinion of Commissioner Wilson in the matter of Illumina/Grail, Dkt. 9401 (tracing applicability of Brown Shoe standard in vertical cases), available at https://www.ftc.gov/system/files/ftc_gov/pdf/d09401wilsonconcurringopinion.pdf; see also Illumina, at 15 (noting unresolved issue).

8 The Antitrust Division’s victory in blocking a merger of two book publishers, United States v. Bertlesmann SE et al., 21-cv-02886 (D.D.C. Nov. 7, 2022), related to competition for best-selling authors, not employees.

9 This “arms race” discussion did not appear in the draft of the 2023 Guidelines.

10 Horizontal Merger Guidelines, Dep’t of Just. and Fed. Trade Comm’n, Aug. 19, 2010, https://www.ftc.gov/sites/default/files/attachments/merger-review/100819hmg.pdf.